Estate planning is a crucial aspect of financial management, yet it is often overlooked until it becomes absolutely necessary. Understanding when and how to plan your estate can save your loved ones a great deal of time, stress, and potential financial hardship. This comprehensive guide aims to demystify estate planning, provide actionable steps, and offer real-world examples to help you get started.

Introduction to Estate Planning

What is Estate Planning? Estate planning is the process of arranging for the management and disposal of a person’s estate during their life and after death. It involves a variety of tasks, including writing a will, setting up trusts, making charitable donations, and planning for estate taxes.

Why is Estate Planning Important? Proper estate planning ensures that your assets are distributed according to your wishes, reduces the burden on your family, and can help minimize taxes and legal fees. It can also provide peace of mind by clearly outlining your wishes for end-of-life care and guardianship of minor children.

When is the Right Time for Estate Planning?

Starting Early The best time to start estate planning is now. Even if you are young or do not have substantial assets, planning early can provide benefits in the long term. Key life events such as marriage, having children, or purchasing a home should prompt a review and update of your estate plan.

Estate planning is an important and everlasting gift you can give your family. And setting up a smooth inheritance isn’t as hard as you might think.

Suze Orman Major Life Changes Whenever you experience significant life changes, it’s essential to revisit your estate plan. These changes include marriage, divorce, the birth of a child, significant changes in financial status, or the death of a beneficiary.

As You Age As you approach retirement, estate planning becomes even more critical. At this stage, you should focus on ensuring that your retirement savings, investments, and other assets are protected and will be distributed according to your wishes.

Key Components of an Estate Plan

1. Will A will is a legal document that outlines how your assets will be distributed after your death. It allows you to designate beneficiaries, name guardians for minor children, and appoint an executor to manage your estate.

2. Trusts Trusts are legal arrangements that allow you to transfer assets to beneficiaries, often with conditions attached. Trusts can be used to minimize estate taxes, protect assets from creditors, and ensure that beneficiaries receive assets in a controlled manner.

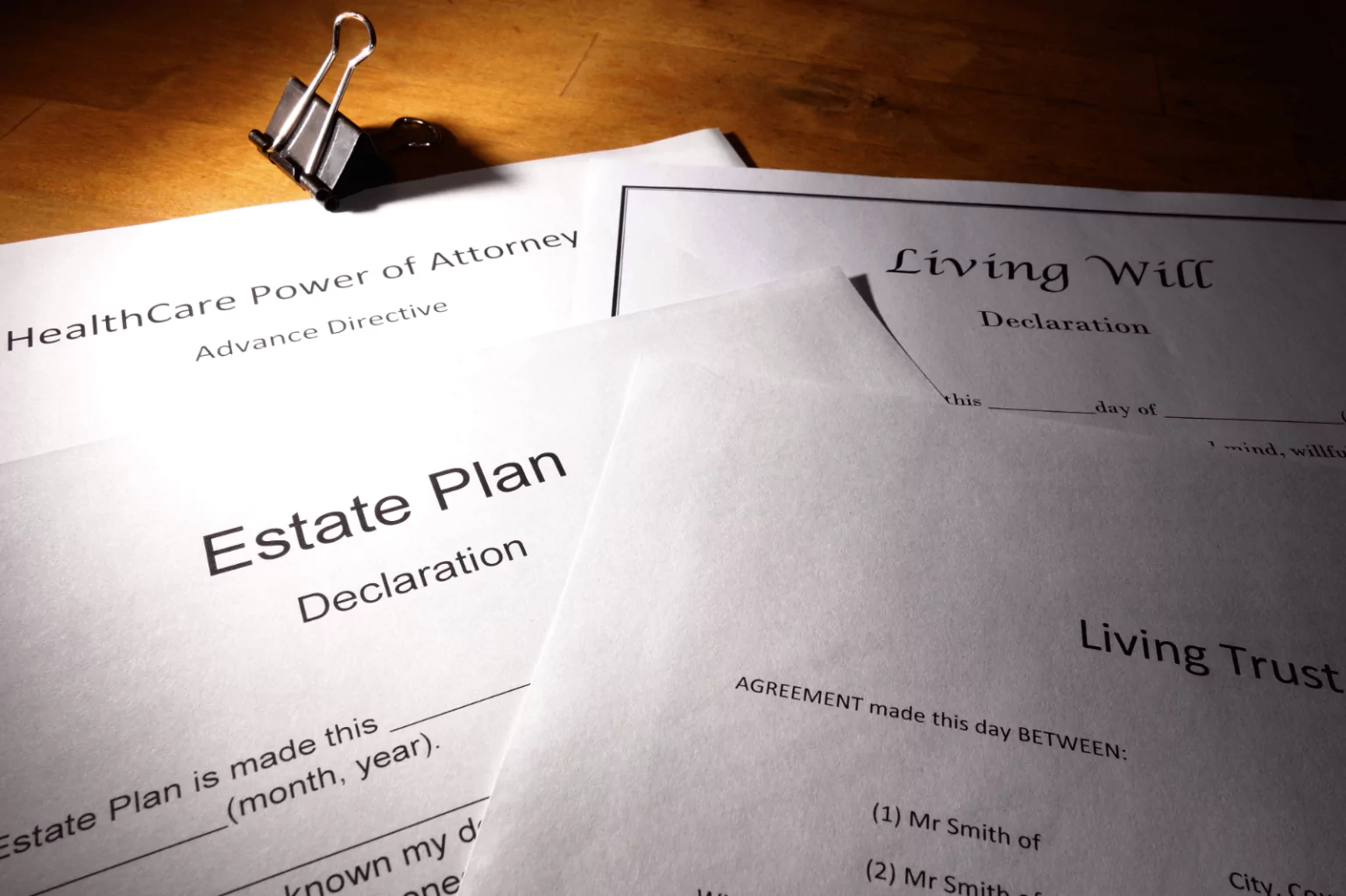

3. Power of Attorney A power of attorney grants someone you trust the authority to make financial and legal decisions on your behalf if you become incapacitated. There are different types of powers of attorney, including general, durable, and medical.

4. Healthcare Directives Healthcare directives, including living wills and healthcare powers of attorney, outline your wishes for medical care if you become unable to communicate your decisions. These documents can specify your preferences for life-sustaining treatment and other critical medical decisions.

The best time to start estate planning is now. Don’t wait until it’s too late to make your wishes known.

5. Beneficiary Designations Ensure that your retirement accounts, life insurance policies, and other financial accounts have up-to-date beneficiary designations. These designations override instructions in your will and directly transfer assets to the named beneficiaries.

Steps to Create an Estate Plan

1. Take Inventory of Your Assets Start by listing all your assets, including real estate, personal property, bank accounts, investments, retirement accounts, and insurance policies.

2. Determine Your Goals Consider what you want to achieve with your estate plan. Common goals include providing for your family, minimizing taxes, supporting charitable causes, and ensuring your wishes are honored.

3. Consult with Professionals Estate planning can be complex, and it’s advisable to seek help from professionals such as estate planning attorneys, financial advisors, and tax experts. They can help you navigate the legal and financial intricacies and ensure your plan is comprehensive.

4. Draft the Necessary Documents Work with your attorney to draft the necessary documents, including your will, trusts, power of attorney, and healthcare directives. Make sure these documents are legally sound and reflect your wishes.

5. Review and Update Regularly Your estate plan should be a living document that evolves with your circumstances. Regularly review and update your plan to reflect changes in your life, financial situation, and relevant laws.

Real-World Examples

Example 1: The Smith Family The Smiths, a middle-aged couple with two children, realized the importance of estate planning when they bought their first home. They created a will, set up a trust for their children’s education, and designated guardians for their children. They also established a healthcare directive to outline their medical wishes.

Example 2: Jane Doe Jane Doe, a single professional with significant assets, focused her estate planning on minimizing taxes and supporting charitable causes. She set up a charitable remainder trust, updated her beneficiary designations, and established a durable power of attorney to manage her financial affairs if she becomes incapacitated.

Important Considerations

Taxes One of the key considerations in estate planning is understanding and planning for potential taxes. Estate taxes, inheritance taxes, and gift taxes can significantly impact the value of your estate. Consulting with a tax professional can help you develop strategies to minimize these taxes.

Legal Requirements Estate planning laws vary by state, so it’s crucial to ensure that your documents comply with local laws. An experienced estate planning attorney can help you navigate these requirements.

Digital Assets In today’s digital age, it’s essential to include digital assets in your estate plan. This includes online accounts, social media profiles, and digital files. Ensure that your executor has the necessary access and instructions to manage these assets.

Resources and Tools

Online Resources Websites like Nolo and LegalZoom offer valuable information and tools for estate planning. These resources can help you understand the basics and provide templates for essential documents.

Financial Institutions Many banks and financial institutions offer estate planning services. For example, Bank of America provides trust and estate services to help you manage and distribute your assets.

Professional Associations Organizations like the American Bar Association and the Financial Planning Association offer resources and directories to help you find qualified estate planning professionals.

Final Thoughts

Estate planning is an ongoing process that requires careful consideration and regular updates. By taking the time to create a comprehensive estate plan, you can ensure that your assets are managed and distributed according to your wishes, provide for your loved ones, and achieve peace of mind.